The Thesis in 60 Seconds

The mainstream story about real estate right now is rate-doom — high mortgage rates, slowing demand, sellers eating losses. That story isn't wrong. It's just not the luxury story.

Here's the picture from the latest available data :

|

Metric |

Value |

What It Means |

|---|---|---|

|

Travis County sales over $2M |

66 |

UP 44% YoY (vs 46) — top-of-market is accelerating, not cooling — KW Austin / MLS |

|

Travis County sales over $3M |

23 |

UP 21% YoY (vs 19) — KW Austin / MLS |

|

Travis County luxury ($1M+) closings |

252 |

UP 15% YoY (vs 220) — KW Austin / MLS |

|

Travis County luxury list-to-sale % |

94% |

Up 2 pts YoY — pricing discipline holding — KW Austin / MLS |

|

Travis County luxury avg DOM |

54 days |

UP 8% YoY (vs 50) — selling steadily, not speeding up — KW Austin / MLS |

|

Cash transactions (luxury) |

~38% |

Rates barely factor in roughly 4 of every 10 deals — secondary / team observation |

|

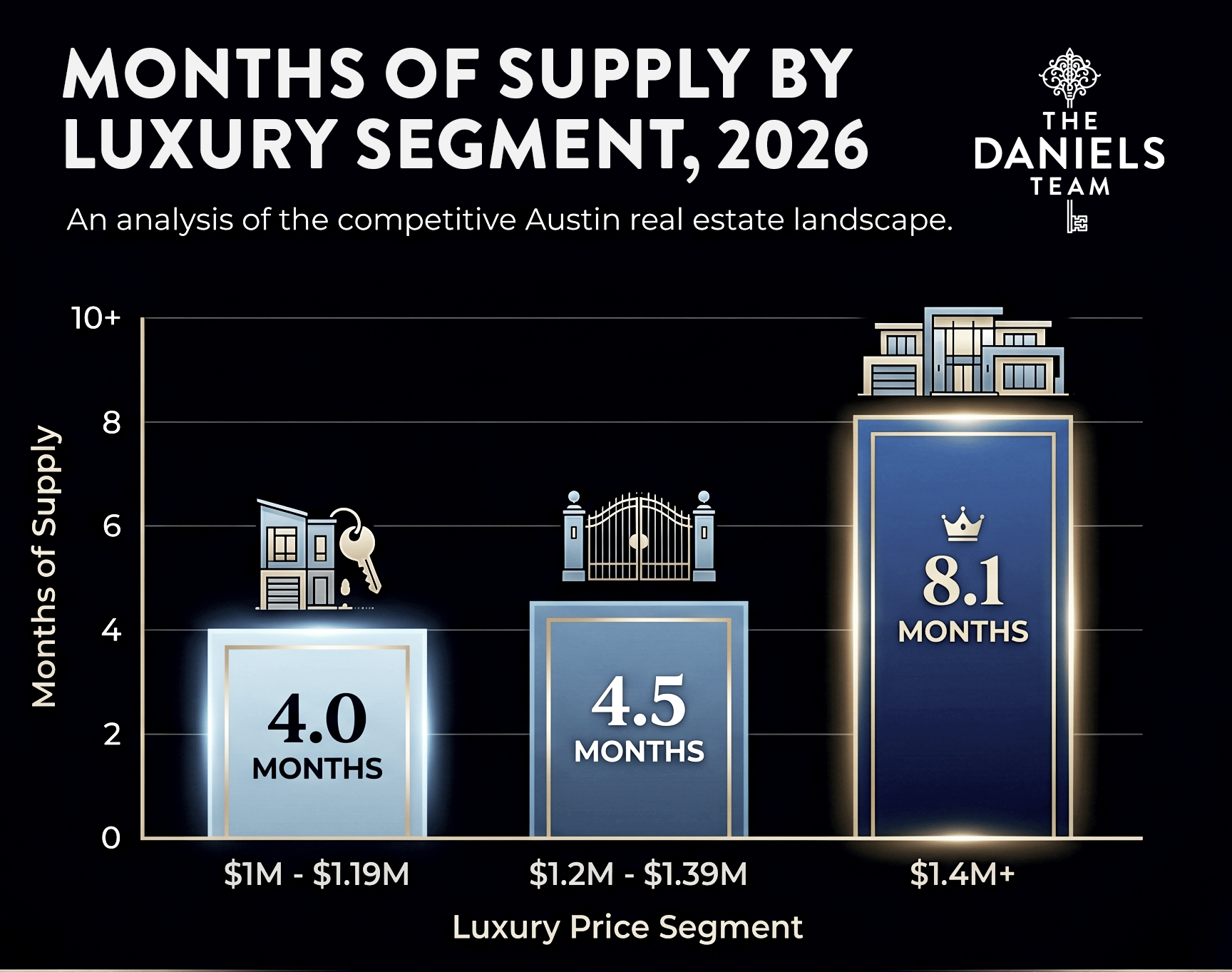

Months of supply ($1M+ overall) |

~6.0 months |

Loosened from earlier in the year — buyer room is returning — Apr 2026, secondary |

|

$1M – $1.19M segment supply |

~4.0 months |

Tightest luxury tier — competitive at entry-luxury — Apr 2026, secondary |

|

$1.2M – $1.39M segment supply |

~4.5 months |

Balanced — Apr 2026, secondary |

|

$1.4M+ segment supply |

~8.1 months |

Buyer leverage at the top end — Apr 2026, secondary |

|

Median luxury sale price |

~$1.34M |

Down ~2.7% YoY — Apr 2026, secondary |

The number that should reframe your thinking: sales over $2M up 44% year over year. That's not a soft-market number — the very top of Austin's market is accelerating even as inventory loosens lower down. The rate-doom narrative simply doesn't fit the $1M+ data.

Why Cash Buyers Don't Care About 7% Rates

The first half of the explanation is the easy one: roughly 38% of luxury deals are all cash. Almost four in ten luxury buyers don't carry a mortgage on the property at all, which means the rate environment doesn't factor into their decision.

Who are these buyers?

-

Relocators with prior equity — selling a Bay Area or NYC primary home releases $1-3M in equity that rolls into a cash purchase here

-

Business sale liquidity events — a private business sale or stock vesting moment converts to a primary or vacation property

-

Generational wealth — family-office or inherited capital that operates on its own time horizon

-

Equity rollover from prior Austin sales — locals trading up using equity built during the 2020-2022 run

Lindsey's been saying it for months: "cash buyers are coming out of the woodwork." It's exactly what we're seeing on the ground. Until the share of cash deals drops meaningfully, rate movement has less effect on luxury demand than headlines suggest.

Why Mortgaged Luxury Buyers Don't Care That Much Either

The harder explanation is for the 62% who do finance. The short version: at $1M+, the buyer typically has high income elasticity, and the strategies around financing get more creative.

A few things are happening at once:

-

The payment delta is real but absorbable. Moving from 5% to 7% on a $1M loan adds roughly $1,300/month — that's real money but not deal-killing money to a $500K+ household income

-

Jumbo loans, ARMs, and asset-collateralized lending are way more common at this tier. A 7-year ARM at 5.875% feels very different than a 30-year fixed at 7%

-

Time horizons are longer. Luxury buyers typically expect to own 7-10+ years. Refi optionality matters more than the entry rate

-

"Marry the home, date the rate" — at this price point, the qualified buyer doesn't actually believe today's rate is forever

That last one is what makes the rate-doom narrative such a poor fit for luxury. The buyer making a $1.5M decision is making it on a 10-year time horizon, and almost everyone we talk to expects to refi somewhere along the way.

The Dripping Springs / Hill Country Sub-Story

If you want a microcosm of the trend — and its nuance — look at the Hill Country. In Hays County (the broader Dripping Springs / Wimberley / Buda corridor), luxury values are firming even as volume swings month to month. The May 2026 average $1M+ sale price came in at $1.41M, up 6% year over year, and luxury homes are still selling fast — 41 days on market, quicker than the Travis County luxury average. Closed $1M+ volume was lighter in May (31 sales) than the spring peak, which is what you'd expect from a thinner, lumpier high-end market where a handful of transactions move the monthly number.

That's the real Hill Country story: a small, supply-constrained luxury pool where prices hold and quality listings move quickly, even when month-to-month closing counts bounce around. The $1.2M+ tier is especially insulated — limited acreage with views, finite buildable land, and a lifestyle premium that doesn't compress with rates. We covered this in detail in our Dripping Springs relocation guide — the same dynamic shows up across Spicewood, Lakeway, and parts of Bee Cave.

What This Means for Buyers vs. Sellers

If you're a buyer: Pay attention to your specific segment. $1M – $1.19M is competitive right now — be ready to move, be ready to negotiate on terms more than price. $1.4M+ has real leverage — there are deals being made in that range that wouldn't have been possible in 2021 or 2022.

If you're a seller: Price realism wins right now. Well-priced luxury is still closing quickly — but with inventory loosening to roughly six months at $1M+, the market is rewarding accurate pricing, not aspirational pricing. Travis County luxury is closing at about 94% of original list price (up two points year over year), which tells you buyers — especially the cash buyers who know the market intimately — are paying for homes priced to the comps, not to the wish list.

The bigger frame — "luxury at all price points": Austin's luxury market has stratified. There's a $1M lane, a $1.5M lane, a $3M+ lane, and the lifestyle/Hill Country lane. Each behaves a little differently. The single biggest mistake we see right now is buyers and sellers reasoning about "the Austin luxury market" as one thing instead of figuring out which lane they're actually in.

The Forward-Looking Call

If mortgage rates drop 50-100 basis points (from current 6.5-7% to 5.5-6%), most market analysts expect a 15-20% surge in buyer activity. The pent-up demand is real — current pricing already reflects this rate environment, and any meaningful relief unlocks demand quickly.

Translation: the buyer who acts now is the buyer who avoids the bidding war on the way down. We've been telling clients for the last month that the next 90 days look like the best buying window in the cycle for $1.4M+ properties, with the caveat that $1M-$1.19M is already competitive.

We could be wrong — markets are unpredictable, and the Fed is one announcement away from changing the picture. But the data is the data, and right now the data doesn't match the doom narrative.

Frequently Asked Questions

Is now a good time to buy luxury real estate in Austin? For $1.4M+, yes — buyers have meaningful leverage and inventory is high. For $1M-$1.19M, the market is competitive but not at peak frenzy. The timing depends more on your segment than on rates.

How are interest rates affecting Austin luxury real estate? Less than you'd expect. 38% of Austin luxury deals are cash, and the financed buyers in this tier have more flexibility (jumbo loans, ARMs, longer hold periods). The rate environment matters, but it isn't the dominant factor it is at lower price points.

Are luxury home buyers in Austin using mortgages or paying cash? Roughly 62% mortgaged, 38% cash, as of early 2026. That cash share has stayed stable through the rate cycle.

Will the Austin luxury market cool down in 2026? The data through May 2026 doesn't support a broad cooling thesis at the top of the market — sales over $2M are up 44% year over year and $1M+ closings are up 15%. Inventory has loosened (roughly six months at $1M+), which gives buyers more room and lengthens days on market in some tiers, but that's a normalizing market, not a cooling one. A meaningful downturn would require a different macro shock than rate movement alone.

What's the best price segment to enter the Austin luxury market? If you're a primary residence buyer, $1.4M-$1.8M currently offers the best combination of inventory and leverage. If you're under $1.2M and competing against other primary buyers, expect more competition and faster moves.

Want to Talk Through Your Move?

If you're sitting on the sidelines because the narrative made you nervous, the conversation is worth having. We do this for a living, we live in the market every day, and we'll tell you straight whether your hesitation is justified or just headlines.